How Are REIT Street Rents Outpacing Achieved Rents in 2025?

Download TractIQ’s exclusive Q2 report to see which operators regained pricing power — and what it means for your portfolio.

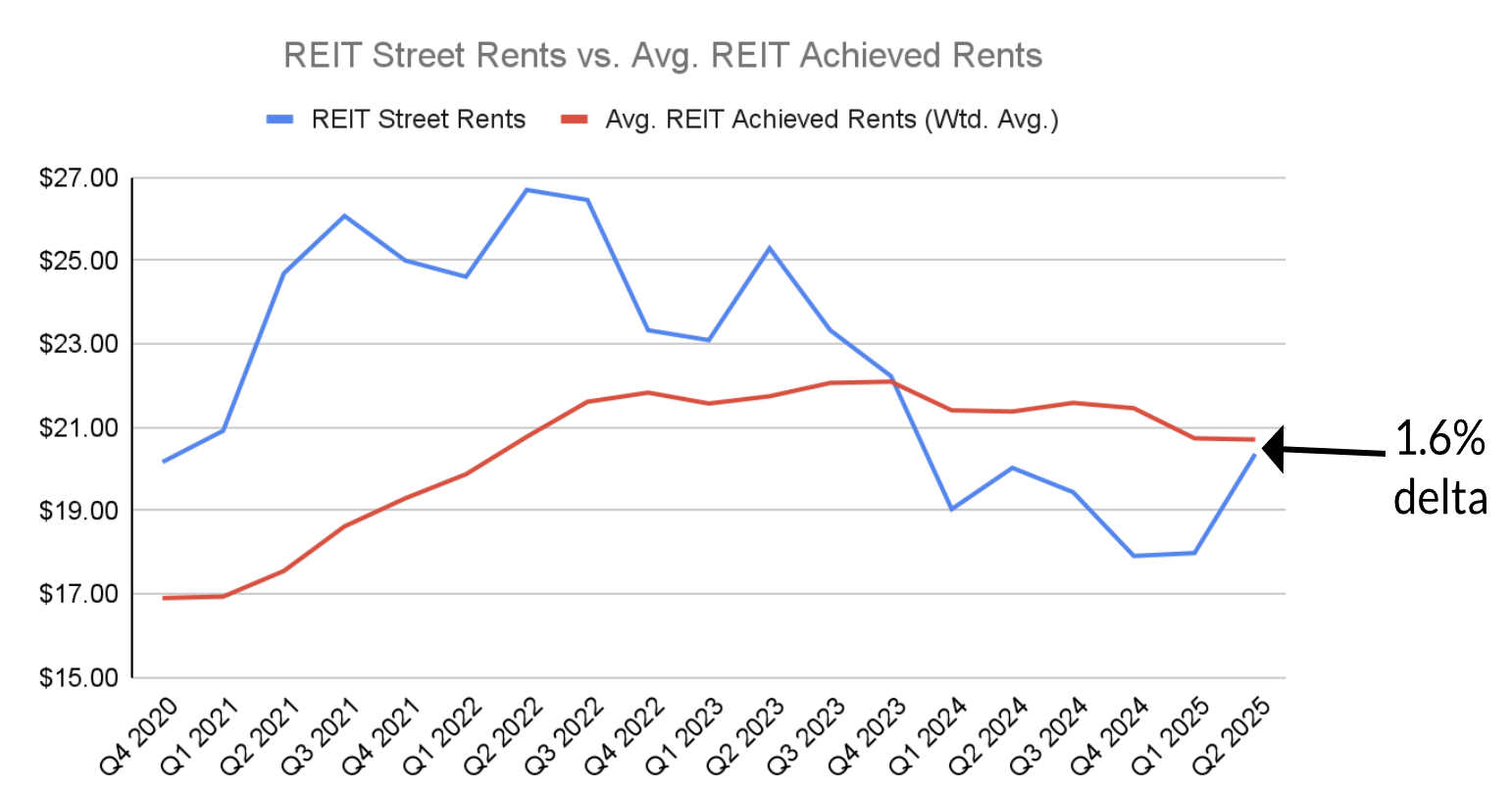

Key Q2 2025 insights - Data at a glance

Advertised Rates

$20.36

+1.7% YOY (vs $17.99 in Q1)

Street rent growth is rebounding — early signs of pricing power returning.

Street rents are regaining momentum after several quarters of decline.

Advertised rates averaged $20.36 in Q2 2025,

up 1.7% YOY versus $17.99 in Q1—an early signal of

pricing power returning in high-demand metros.

Achieved Rates

$20.71

−3.1% YOY (vs $20.74 in Q1)

Post-pandemic churn normalizing as higher in-place tenants cycle out; move-in rates stabilizing.

Achieved rates averaged $20.71 in Q2 2025, a

3.1% YOY decline. This reflects normalization as

pandemic-era, higher in-place tenants cycle out and move-in pricing stabilizes—healthier turnover and more

predictable revenue mix.

Street vs Achieved Delta

1.7%

↓ 73.6% YOY (from 6.3%)

The narrowest spread in years → higher predictive accuracy for underwriting (esp. Extra Space & NSA).

The gap between street and achieved rents compressed to

1.7% in Q2 2025—a

73.6% narrowing YOY from 6.3%.

This convergence strengthens street rates as a leading input for underwriting,

especially for portfolios like Extra Space and NSA.

Discount Rate

23.7%

+13.8% YOY (vs 23.6% in Q1)

Discounting remains steady, reflecting competitive pressure and muted demand despite rate shifts.

Discounting remained steady at

23.7% in Q2 2025

(vs 23.6% in Q1; +13.8% YOY).

The pattern suggests muted demand but persistent competitive pressure as operators balance occupancy

objectives with disciplined price controls.