Self-storage REITs ended 2025 on firmer footing than they began the year.

Operating trends improved relative to 2024, and management teams broadly expect another step forward in 2026 as new supply continues to moderate. Here are some highlights for the quarter:

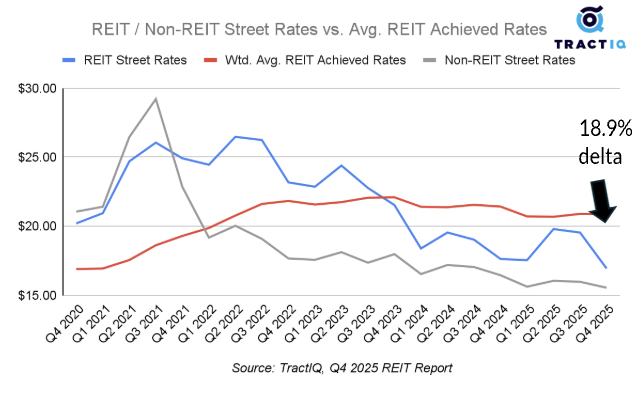

Key Self-Storage Insights

Street-rate declines persisted in Q4, but continues to stabilize. REIT street rates declined 3.9% YoY in Q4 2025, a much more modest drop than the 18.9% YoY decline recorded in Q4 2024.

Achieved rate pressure eased. REIT achieved rates declined 2.5% YoY, representing the smallest YoY decline since Q3 2024. Discounting remained elevated, and several REITs cited higher-than-normal pricing competition from both sophisticated and non-sophisticated operators.

Occupancy showed one of the clearest signs of an inflection point. Weighted average REIT occupancy declined QoQ, but increased 0.3% YoY — the first YoY occupancy gain since Q4 2021. This suggests the sector is moving from deterioration to stabilization.

Expense growth moderated, and NOI may be nearing a trough. NSA was the only REIT to report a year-over-year expense decline (-0.8%), while Extra Space’s expense growth slowed materially from earlier in 2025. Extra Space was also the only REIT to post positive same-store NOI growth in Q4 at 0.1% YoY — the first positive YoY NOI result among the REITs since TractIQ started tracking the data in Q2 2024.

Recovery remains highly market-specific. Florida and Texas markets continued to show weakness, with Tampa, North Port-Sarasota, Houston, and San Antonio among the weakest for YoY street-rate growth. By contrast, St. Louis, Richmond, Boston, and Louisville posted relative strength.

Achieved Rates

Representing the smallest YoY decline since Q3 2024.

Street Rates

REIT street rates declined 3.9% YoY in Q4 2025