Why Q1 2026 is a turning point for self-storage REITs

For most of the last two years, self-storage REIT earnings have been a mixed bag — one operator up, another down, occupancy sliding somewhere in the background. Q1 2026 broke that pattern. All five publicly traded self-storage REITs posted same-store revenue growth of 0% or better, the first time that’s happened since 2024. That alone is worth paying attention to, but the story underneath the headline number is more interesting than the number itself.

Same-store revenue and NOI, REIT by REIT

Extra Space Storage led the group at +1.7% same-store revenue growth, with SmartStop close behind at +1.5%. CubeSmart came in at +0.6%, which doesn’t sound like much until you know it ended six straight quarters of negative revenue growth. Public Storage was flat at 0.0%, and NSA returned to positive territory at +0.2%.

NOI mostly tracked revenue. EXR, NSA, SmartStop, and PSA all posted positive same-store NOI growth. CubeSmart was the outlier at -1.5%, and the reason is specific: advertising expense jumped 54% year over year, and personnel costs rose 7.2%. Revenue can turn positive while NOI still lags if a REIT is spending harder to get there.

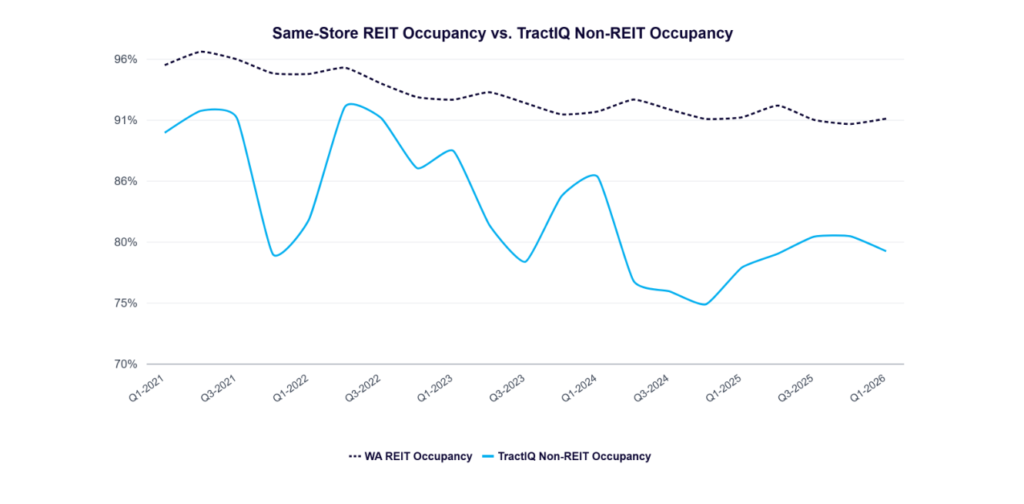

Occupancy and move-in volumes

Sector-wide weighted average same-store occupancy landed at 90.9% in Q1 2026, down just 0.2 pp year over year and about 5.1 pp below the 2021 peak. That’s a small enough move to read as stabilization rather than a continued slide. EXR (93.0%) and SmartStop (92.3%) are running ahead of the group, and NSA was the only REIT to post occupancy expansion, up 0.9 pp YoY.

Move-in volumes back that up. EXR’s net move-ins jumped 58% YoY to 6,375, its strongest quarter since Q1 2024. CubeSmart posted 1,903 net move-ins, its highest volume since Q1 2023 and its largest year-over-year gain since 2021. EXR’s move-in rate turned positive year over year for the first time on record, and even PSA’s move-in rate decline, at -2.4%, was its smallest since the data series started in 2020. Move-ins tend to lead revenue by a quarter or two, so this is one of the more useful numbers in the whole report.

The Public Storage-NSA merger

The other headline from the quarter: on March 16, 2026, Public Storage announced an all-stock merger with National Storage Affiliates worth roughly $10.5 billion. It would fold 1,000+ NSA wholly-owned stores into PSA’s existing 3,000+ store platform, and it pushes PSA deeper into secondary and tertiary markets where NSA already has a footprint. Closing is expected in Q3 2026. If it goes through, it’s one of the larger consolidation moves the sector has seen, and it’ll be worth watching how it changes PSA’s exposure outside the top MSAs.

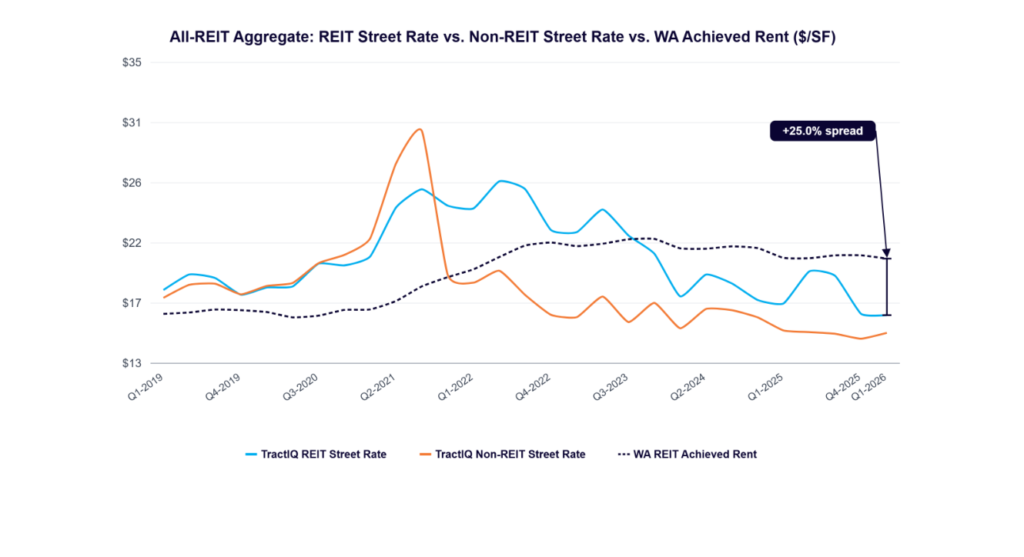

Reading the achieved-rate vs. street-rate gap

One number that’s easy to miss in the earnings decks: the gap between what REITs are actually collecting (achieved rate) and what they’re advertising to new customers (street rate) widened again this quarter. REIT weighted-average achieved rent hit $20.66/SF against a TractIQ-tracked street rate of $16.52/SF, a $4.14/SF spread, up from +19.2% a year ago to +25.0% now. That’s not uniform across markets. Sunbelt metros like Austin, San Antonio, and Dallas are still showing street rate weakness, while supply-constrained markets like Los Angeles, Minneapolis, and San Jose posted positive year-over-year growth. If you’re underwriting a deal, which side of that split your market falls on matters more than the sector average.

The full report breaks all of this down REIT by REIT and MSA by MSA — get it here. For more on how street and achieved rates diverge across markets, see our self-storage REIT source data page, or check self-storage market data for the broader picture. If you want to talk through what this means for a specific deal, book a demo.